Blue Ocean Strategy for Startups. How to Swim Past the Competition

Picture this: You’ve built an amazing mobile app, but so have a dozen other startups. The app stores are crowded, competition is fierce, and it feels like you’re all fighting over the same users. It’s a bloodbath, quite literally a red ocean of rivals. Now imagine sailing into open, clear waters with no competitors in sight. That’s the promise of Blue Ocean Strategy: creating an untapped market space where you make the competition irrelevant. In this article, we’ll explore what Blue Ocean Strategy is, how it differs from traditional competitive strategies, and how startup founders (B2B or B2C) can apply it to mobile apps. We’ll look at inspiring examples, from Uber to Slack, and break down practical steps to help you chart your own course into a blue ocean of opportunity.

What Is Blue Ocean Strategy?

Blue Ocean Strategy is a business approach introduced by W. Chan Kim and Renée Mauborgne in the mid-2000s. The core idea is simple: instead of competing head‑to‑head in overcrowded industries (the red oceans), find or create new market space (a blue ocean) where you can sail freely without battling sharks (aka competitors) over the same prey (customers). In a red ocean, companies fight a zero-sum game over a fixed demand: one company’s gain is another’s loss. In a blue ocean, you generate new demand by offering extraordinary value that no one else is providing. As the creators of the concept put it, Blue Ocean Strategy is “the simultaneous pursuit of differentiation and low cost to open up a new market space and create new demand”. In other words, a blue ocean move isn’t just about being different – it’s about being different while delivering great value at low cost, so that you unlock a whole new pool of customers.

To illustrate, the authors often use a vivid metaphor: “Think of competitors as sharks. That’s why the red ocean is red, it’s full of blood from intense competition”. By contrast, a blue ocean is wide open and calm, symbolizing the vast opportunity when you’re not surrounded by competitors. Blue ocean companies don’t play the game of outdoing rivals on the same metrics; they change the rules of the game entirely. They don’t compete – they create. For a resource-strapped startup, this approach can be a game-changer. Instead of pouring all your energy into beating established rivals (who likely have more money and users), you look for a completely new space where you can be the leader from day one.

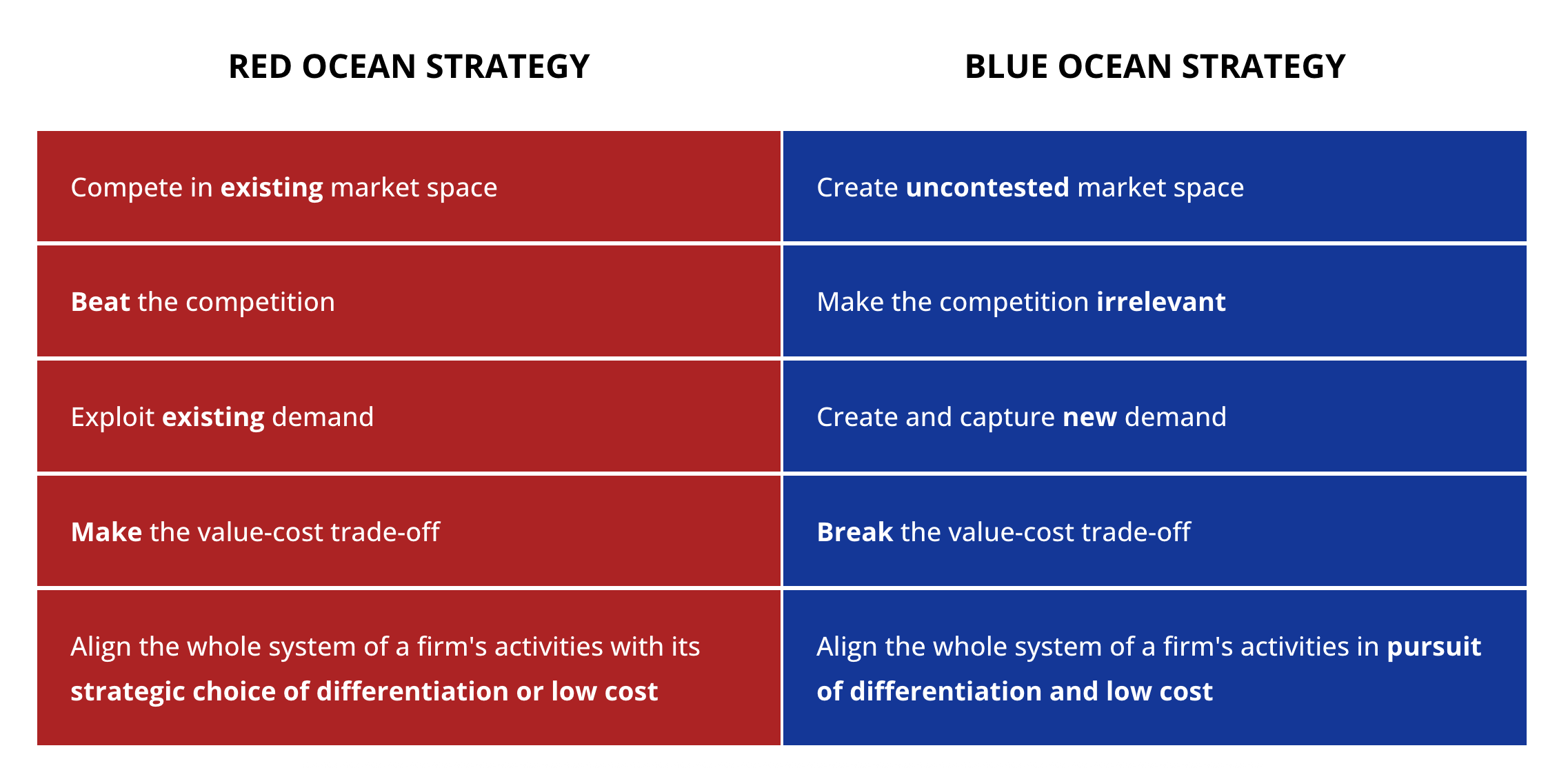

Red Ocean vs. Blue Ocean: Key Differences

It’s helpful to compare traditional strategy with blue ocean strategy to see how fundamentally they differ. In a nutshell, red-ocean thinking is about fighting to win in an existing market, whereas blue-ocean thinking is about creating a new market so you don’t have to fight at all. Here are some key differences:

Market Space: Red ocean strategy focuses on competing in the existing market space, where industry boundaries are defined and crowded. Blue ocean strategy is about creating an uncontested market space, an area no one has claimed yet. For example, Cirque du Soleil invented a new form of live entertainment that wasn’t quite circus or theater.

Approach to Competition: In red oceans, companies try to beat the competition and take a larger share of a limited pie. In blue oceans, the goal is to make the competition irrelevant by offering such a leap in value that others aren’t even playing the same game. If you’re successful, competitors either can’t catch up easily or they ignore you because you’re operating in a different realm altogether.

Demand: Red ocean strategy exploits existing demand, fighting over customers who are already in the market. Blue ocean strategy creates and captures new demand, bringing new customers into the fold. Often this means turning non-customers (people who weren’t using any solution in your category) into customers by fulfilling an unmet need.

Value–Cost Trade-off: Traditional strategies typically accept a value-cost trade-off – you either differentiate your product (and usually charge more) or compete on cost by offering a no-frills service. Blue ocean strategy seeks to break that trade-off. Blue ocean innovators aim to deliver higher value while keeping costs low, achieving what Kim and Mauborgne call “value innovation”.

Whole Company Alignment: In red oceans, the company’s activities align with a strategic choice of either differentiation or low cost. In blue oceans, all activities align in pursuit of both differentiation and low cost. Every part of the business: product design, pricing, marketing, is orchestrated to create that unique high-value, low-cost offering.

These differences highlight why blue ocean strategy can be so powerful. Rather than duking it out in a saturated app category (say, yet another food delivery or photo-sharing app), a startup that finds a blue ocean is essentially writing its own ticket. You’re not entering an existing race; you’re starting a new one that only you are running. As a result, profits and growth in blue oceans can be rapid and sustainable because you face little to no initial competition. Of course, nothing stays competition-free forever – if you’re successful, others will eventually try to imitate you. But by then, you’ll have the advantage of being the pioneer with a head start.

Why Blue Ocean Strategy Matters for Startups

For startups, the Blue Ocean approach is more than just strategic theory, it can be a survival tactic and a formula for outsized success. Here’s why:

Avoiding Head-to-Head Battles: Most startups don’t have the deep pockets or user base to go toe-to-toe with big incumbents in a crowded market. A blue ocean strategy frees you from this trap. Instead of trying to out-Uber Uber or be a slightly better Instagram, you focus on an area where no one is competing yet. By carving out a new niche with no competitors, you sidestep the resource-draining arms race of feature-by-feature competition. This was one secret to Slack’s rise. They didn’t directly take on email or existing enterprise chat apps at first; they created a new, fun, integrated way for teams to communicate, effectively defining a new category of workplace collaboration. Slack’s founders positioned it so differently that, for a while, it wasn’t compared to anything else, it was just Slack, and it became the go-to tool for teams almost by default.

Unlocking New Customer Pools: Blue ocean thinking pushes you to look at who isn’t your customer yet, and ask why. Maybe they find current solutions too expensive, too complicated, or simply not addressing their specific need. By innovating for these non-customers, you can unlock a wave of new demand. For example, Airbnb’s founders didn’t target people who were already loyal hotel customers; they targeted travelers who wanted a more personal, affordable experience and homeowners with spare space. In doing so, Airbnb transformed countless ordinary people into hosts and attracted travelers who previously might not have traveled as often due to cost – a completely new market segment for hospitality.

Changing the Game and the Metrics: Competing in an existing market often means everyone is improving along the same dimensions (faster car, bigger screen, more toppings on a pizza, etc.). A blue ocean strategy encourages you to change the metrics of competition. You might eliminate features the industry takes for granted and add new ones that haven’t been offered. The result is a product or app that isn’t comparable to the status quo. Think about how Cirque du Soleil did away with costly circus staples like animal acts and star clowns, and added elements from theater and dance. The result was a brand-new entertainment format. They appealed to adults willing to pay theater prices for a sophisticated circus experience, leaving traditional circuses to compete over the family/kid market. A similar concept in apps might be, say, eliminating the bloated features common in enterprise software but adding a social, user-friendly twist that none of the legacy players offer. When you redefine what value means, you make the old value metrics less relevant.

Higher Growth and Profit Potential: Because a blue ocean is uncontested, a startup can capture a large share of new customers quickly without costly marketing wars. Often, blue oceans are very profitable because you face no price pressure initially – you’re the only one satisfying the demand. One study of blue ocean moves found companies in new markets often achieve strong, profitable growth rapidly, whereas red-ocean battles tend to squeeze margins over time. For instance, when Netflix pioneered mailing DVDs via subscription and later streaming, they enjoyed years of growth with relatively little direct competition. By the time competitors woke up, Netflix had millions of subscribers and a formidable lead in technology and content. For a startup founder, that kind of head start can make the difference between becoming the category king or just becoming roadkill in a price war.

In short, Blue Ocean Strategy matters for startups because it’s about working smarter, not harder. Instead of spending your precious capital on ads to steal customers from others, you spend your energy on innovation, creating value where there was none, and in doing so attracting customers who had been overlooked. It’s a chance to set the rules on your own terms. Of course, it requires a mindset shift: you have to stop obsessing over competitors and instead obsess over customers. But for those who pull it off, the rewards can be huge.

Blue Ocean Strategy in Action: Famous Examples

Sometimes the best way to grasp this concept is to see it in action. Many successful companies, including startups that grew into giants, have employed Blue Ocean Strategy to great effect. Here are a few canonical examples that demonstrate how blue oceans are created:

Cirque du Soleil, Reimagining the Circus: Cirque du Soleil is a textbook example of Blue Ocean Strategy. In an industry (circuses) that was declining and crowded with similar offerings, Cirque created a new form of entertainment by blending circus arts with theater, eliminating expensive aspects (no animals, no celebrity ringmaster) and adding new elements like artistic storytelling and live music. The result? They drew in a completely new adult audience willing to pay premium prices for a sophisticated show, far beyond what traditional circuses could charge. Since its start in the 1980s, over 155 million people have attended Cirque du Soleil shows worldwide – all achieved without competing on the same old circus turf. They made the competition irrelevant because Ringling Bros. and other circuses weren’t even playing in the same space anymore.

Uber, Transforming Transportation: When Uber arrived in 2010, it didn’t set out to be just another taxi company; it changed the rules of the game. Uber’s blue ocean strategy focused on providing a fast, convenient car service on-demand via mobile app. This eliminated big friction points that people just accepted with taxis: standing on a street corner to hail a cab (or calling a dispatcher and wondering when the car would show up), uncertainty about pricing, and the need to carry cash. By leveraging smartphone technology, Uber created a seamless user experience for getting a ride, one that was often more reliable and pleasant than traditional cabs. Importantly, Uber initially targeted a market gap: in its early days it offered black-car services through an app, tapping into an unmet demand for upscale, on-demand rides that taxi services weren’t fulfilling. There was already “a sizable demand for on-demand transportation” at the high end, but no easy app-based way to get it. Uber stepped into that blue ocean, and by the time competitors reacted, Uber had redefined urban transportation. The company made the idea of hailing a ride via app the new norm, leaving traditional taxi companies struggling to catch up in a game Uber invented.

Airbnb, Unlocking an Untapped Hospitality Market: Another startup-turned-giant, Airbnb created a blue ocean by seeing potential where others saw none. In 2008, nobody thought renting an air mattress in someone’s living room was a business opportunity, except Airbnb’s founders. They recognized an underutilized resource (spare rooms and homes) and an unmet desire among travelers for affordable, homey, authentic places to stay. Instead of competing with hotels on hotels’ terms, Airbnb offered a completely different value proposition: allowing regular people to earn money by renting out their homes, and giving travelers the chance to stay in unique local places often cheaper than hotels. This peer-to-peer model disrupted the traditional hospitality industry. Airbnb effectively created new customers: travelers who wanted a more personal experience than hotels offered, and homeowners who became hospitality providers without any hotel investment. It was a classic blue ocean play – no direct competition at the start because no one else was doing it. Today, Airbnb is a global force, and while it eventually attracted competitors, it had years of uncontested growth to establish its brand and network.

Slack, Redefining Team Communication: In the B2B SaaS arena, Slack is often cited as a blue ocean success. When Slack launched in 2013, corporate communication was dominated by email and a few clunky enterprise chat tools. Instead of trying to compete with email providers or enterprise software giants directly, Slack took a fresh approach: it created a fun, easy-to-use messaging platform that felt more like a consumer chat app, combined with powerful integrations to other work tools. Slack’s value was not just in messaging, but in organizing team communications into channels, being searchable, and integrating with everything from Google Drive to developer tools. They essentially eliminated the formal, slow aspects of email and raised the game by making workplace communication real-time, transparent, and even enjoyable. By the time Microsoft and others woke up and launched rival products, Slack had already become the go-to solution for thousands of teams, riding the blue ocean it created. It captured a huge user base (many of whom were new to using a dedicated comms tool beyond email) and forced even Microsoft to change its strategy, resulting in Microsoft Teams. Slack’s meteoric growth happened because it wasn’t just a little better than email – it was a different and better way to communicate at work, which struck a chord with users and spread virally.

Netflix, Evolving and Creating New Markets: Netflix provides a great example of how a company can keep finding blue oceans over time. First, Netflix reinvented home video rental. Instead of competing with Blockbuster’s huge chain of stores by opening more stores, Netflix mailed DVDs directly to subscribers and crucially eliminated late fees with a flat-rate monthly subscription. This solved major customer pain points (no more trips to the store or penalty fees) and attracted a wave of movie lovers who were disillusioned with traditional rental stores. Once that model succeeded, Netflix didn’t stop, they looked ahead and bet on streaming video when that was an almost untested market. By pivoting to streaming early, Netflix opened up yet another new space, delivering instant content on-demand long before most competitors (and before many customers even knew they wanted it). Finally, as streaming got crowded in later years, Netflix created original content, essentially becoming a studio, to offer entertainment viewers couldn’t get anywhere else. Moves like these kept Netflix in blue oceans for much of its history, allowing it to grow from a tiny startup in the late ’90s to an entertainment behemoth. It’s a reminder that blue oceans aren’t one-time events; companies can continuously seek new blue oceans as technology and markets evolve.

These examples (and many others, from Apple’s iTunes to Nintendo’s Wii) highlight a common theme. The companies didn’t win by playing the same game better; they won by changing the game entirely. They identified gaps or needs that no one was addressing and innovated their way into those gaps. In each case, the “competition” as traditionally defined became irrelevant or secondary.

How to Apply Blue Ocean Strategy to Your Startup

All this talk of Cirque du Soleil and Uber is inspiring, but as an early-stage founder, how can you actually put Blue Ocean Strategy into practice? It’s not as simple as deciding one day to “be innovative.” It requires a mix of creative thinking and strategic tools. Here are some practical steps and tips to help you start charting a blue ocean for your own app:

Spot the Pain Points: Start with deep market research and customer insight. Look at your target domain and ask: What frustrates people about the current options? What could be done better or differently that no one is doing? Often, big opportunities hide in plain sight – those everyday gripes or inefficiencies users just “live with.” For instance, before ride-hailing apps, people accepted the fact that hailing a cab was hit-or-miss and that payment was a hassle. Uber spotted these pain points and leveraged technology to remove them. Do the same in your domain. Read app reviews, talk to users, observe behaviors. Are customers truly happy with existing solutions, or are they tolerating them? If you find widespread annoyance or unmet needs, you’ve found fuel for a blue ocean idea. Remember, blue oceans often come from addressing a problem others have ignored.

Look Beyond Current Users: Don’t just focus on the users every competitor is chasing. Ask who isn’t using any of the current solutions. Why are they sitting on the sidelines? These non-customers can point you to blue oceans. Perhaps they find existing apps too expensive, too complicated, or not tailored to their niche needs. By understanding their reasons, you can craft an offering that brings them on board. For example, think of people who never used personal finance apps because they found them too geeky and time-consuming – that insight led one startup to create a super-simple, automated budgeting app for the non-finance crowd, effectively creating a new user base. Identify the gaps: if millions of potential users out there aren’t using any app in your category yet, find out what’s stopping them and address it. Blue Ocean Strategy explicitly encourages targeting these non-consumers whom incumbents neglect. By designing for them, you can unlock new demand that existing players aren’t capturing.

Apply the Eliminate-Reduce-Raise-Create framework: Here’s a handy tool straight from Blue Ocean Strategy’s playbook. The idea is to systematically brainstorm how you can reconstruct buyer value elements in your industry. Grab a whiteboard and make four lists by asking yourself:

Eliminate: Which factors or features that everyone in the industry takes for granted can you cut out entirely? These might be things customers don’t actually value as much as assumed, or things that add cost/complexity.

Reduce: Which factors should be reduced well below the industry standard because they’re overkill? Maybe apps are all competing on one upping each other with fancy AI that users don’t fully need, you could simplify.

Raise: Which factors should be raised above the standard, by offering much more of something customers do value? E.g. greater simplicity, better customer support, stronger privacy, anything current players skimp on.

Create: Which factors can you create that the industry has never offered? This is the true innovation, features or experiences new to the space.

This ERRC framework forces you to think differently from competitors, rather than just doing more or less of the same. For instance, if you were designing a new educational mobile app, you might eliminate the ads and sign-up friction that plague others, reduce the heavy content bloat, raise the level of personalization or gamification, and create a social learning community feature that no traditional e-learning app has. By the end of this exercise, you should have a rough sketch of a value proposition that’s distinct. It’s essentially your blueprint for a blue ocean product. As Kim and Mauborgne note, answering these four questions can serve as the basis of an action plan to break away from the pack. Don’t be afraid to challenge industry norms here – that’s exactly the point.

Focus on Value Innovation: Always check that your ideas from step 3 actually create a leap in value for the customer and for you. A cool idea that doesn’t clearly excite customers (or that can’t be delivered at a viable cost) won’t float. Blue Ocean Strategy is all about value innovation, meaning you innovate in a way that increases value for buyers while also benefiting your own cost structure. Ensure that the changes you plan (eliminating X, creating Y) either solve a big customer pain or add a significant gain. At the same time, see if they allow you to streamline costs. A classic example is how Yellow Tail wine simplified wine production (reducing cost) but made the taste sweeter and branding simpler to attract casual drinkers (increasing buyer value). For your app, perhaps you can remove expensive-to-maintain features that few use and use those resources to double down on the main feature that does matter to users, for example. The sweet spot is a product that delights customers and is efficient to operate. Keep asking: Are we offering a vastly better experience or solving a major problem, and can we do it sustainably? If yes, you’re on the right track.

Test, Tweak, and Validate: One thing to remember: blue ocean or not, you’re still a startup. That means you should test your assumptions early and iterate. Just because you think an idea is groundbreaking doesn’t mean customers will flock to it. Use lean startup tactics to validate your blue ocean concept. This could mean building a small prototype or landing page to gauge interest, running a pilot with a subset of your target audience, or even creating a simple demo video to see if people bite. The goal is to ensure that the “new value” you plan to offer actually resonates with real users. For example, if your blue ocean hypothesis is that “busy parents will use our app because current solutions are too time-consuming,” test that! Show a group of busy parents a mock-up or do interviews to confirm the pain point and see if your idea appeals. This way, you can refine your unique offering before a full launch. Blue oceans carry uncertainty. You’re doing something new, after all, so staying agile and responsive to feedback is critical. The good news is that because you’re targeting an uncontested need, feedback might reveal huge enthusiasm if you’ve struck the right chord. Listen to what early users love or don’t get about your concept and adjust accordingly.

Be Prepared to Pivot or Persist: As you test, be open to pivoting your strategy without abandoning the blue ocean ethos. Maybe you discover a different untapped need that’s even bigger than the one you first envisioned – don’t be afraid to tack towards it. Blue ocean strategy isn’t a one-time decision; it’s a creative, ongoing search. If early signals show that your idea isn’t working, analyze whether the fundamental concept is off or if it’s just the execution. It might take a couple of iterations to find the exact product-market fit in a new space. That said, when you do see validation – users saying “I’ve been waiting for something like this!” – then double down and move fast to capture the opportunity before others notice. Executing a blue ocean strategy often requires courage and persistence; you might face skeptics who don’t get your vision (incl. investors who ask “But who else is doing this?”). Stick to your convictions if you have evidence that users want what you’re building. After all, Uber’s idea of strangers riding in each other’s cars sounded crazy to many at first. Visionary founders sometimes have to go against conventional wisdom, that’s part of creating a new market.

Educate the Market (Build Demand): In a truly blue ocean, your potential users might not even know they have a need for your product yet, or they don’t understand it. Part of your job is to clearly communicate the value proposition and educate customers on this new solution. When Dropbox introduced the idea of a “folder in the cloud” for file storage, most people didn’t know they needed it, so Dropbox made a simple video and gave away free storage to drive the point home. If your app is doing something novel, craft a compelling story around it. Demonstrate the problem and how your solution is different from anything else. Sometimes this involves content marketing, demos, or creative onboarding to show users the “aha!” moment quickly. The advantage here is that if you pull it off, you aren’t just gaining users – you’re often creating enthusiastic evangelists, because they feel like they’ve discovered something really new and useful. They’ll tell others, and your blue ocean can expand rapidly. Airbnb, for example, grew in large part through word of mouth from travelers delighted by the unique experiences, and hosts excited to earn money, essentially building a community around a new idea in hospitality.

By following these steps, you’re essentially applying a startup lens to Blue Ocean Strategy. It’s about finding that intersection between an unmet need and a bold solution, and then executing smartly. Keep in mind, this strategy doesn’t mean throwing caution to the wind. It should be grounded in insight and iterated on with feedback. However, it does mean being willing to defy the ordinary. You might cut out features that every other app like yours includes by default, or target a user group that conventional wisdom says is “too small” (niche markets can sometimes bloom into very large ones when unlocked). That takes confidence and clarity of vision. But as the examples earlier showed, this is how some of the biggest startup success stories happened. They didn’t win by copying what came before and tweaking one thing; they offered something so fresh that users flocked to them.

Potential Pitfalls and How to Navigate Them

Before we wrap up, a dose of reality: pursuing a blue ocean strategy isn’t a guaranteed slam dunk. There are challenges you should be aware of:

Is There Really an Ocean? – Sometimes what looks like a blue ocean can turn out to be a mirage. You might identify a need that seems large, only to find that not enough customers actually want that new thing, or they’re not willing to change their habits. Always do the homework and validate demand as discussed. Ensure that the “uncontested” space you’re going after isn’t empty just because no one actually cares! The history of startups is littered with products that were technically innovative but solved a non-problem. So, pair your creativity with customer reality checks.

Timing Matters – You could be too early. If the enabling technology or infrastructure for your solution isn’t there yet, the market may not take off. For example, an app that relied on, say, widespread 5G adoption back in 2015 would have been too ahead of its time. Blue oceans often involve some foresight into where trends are going, but be careful not to overshoot. On the flip side, if you’re too late, then chances are it’s not a blue ocean anymore. Monitor technology trends and cultural shifts; sometimes the difference between flop and fabulous is hitting the timing just right when customers are ready for your innovation.

Execution and Imitation – Just because you have a brilliant blue ocean idea doesn’t mean execution is easy. You need to deliver that value innovation reliably. If your app promises a revolutionary service but is constantly crashing or hard to use, customers won’t stick around. Operational excellence and great user experience are still crucial. Also, if your idea is truly good, expect fast followers. The competition won’t remain “irrelevant” forever; they’ll either try to copy you or pivot into your space if they see you gaining traction. That’s why the advice is often to use your head start wisely – build brand loyalty, scale quickly, maybe even secure strategic partnerships or network effects that make it harder for others to just clone your success. For instance, by the time competitors aimed at Netflix’s streaming market, Netflix had not only a huge subscriber base but also proprietary content and algorithms tailored to user preferences, giving it buffers against imitators. Consider what your “moat” will be once others notice your blue ocean.

Resource Constraints – Some blue ocean opportunities might require significant upfront investment or patient capital, which can be tough for early startups. If your vision is very ambitious (say, creating a whole new transportation system or a new hardware device ecosystem), plan for how to get the resources needed. Often, breaking it into smaller steps or proving parts of the concept can help attract investors or partners. Alternatively, think creatively about leveraging existing infrastructure to test your idea on a smaller scale first.

The key is not to be scared off by these challenges, but to approach Blue Ocean Strategy with eyes open. It’s a powerful approach, but not a magic wand. As one source wisely notes, a blue ocean strategy is not a holy grail, but it will lead to success in skilled hands. This means you need to combine the strategy with good execution, adaptability, and a solid team to navigate the uncharted waters.

Conclusion

In the fast-moving startup industry, it’s too easy to get caught in the red ocean of fierce competition, endlessly checking what rivals are doing, adding one more feature to keep up, cutting prices to win a few more users. But the stories of successful startups teach us that truly breakout growth often comes from a different approach: creating your own game rather than playing someone else’s. Blue Ocean Strategy offers a blueprint for exactly that. It challenges you to re-imagine the market, to ask new questions like “Who else could be my customer?” or “What if we stopped doing what everyone else does?” By focusing on new value creation over competition, you can uncover opportunities that others miss.

For a startup founder, this mindset can be incredibly liberating. It shifts your perspective from scarcity (“there are only so many customers, and we all have to fight for them”) to abundance (“there are untapped customers and needs out there, and we can create something just for them”). It encourages bold innovation. The kind that not only sets you apart, but can also change the industry. Companies like Airbnb or Slack achieved success not by being 10% better than the next app, but by being different in kind, delivering unique value that made users think, “Where have you been all my life?”.

So as you work on your startup or mobile app, take a step back and survey the waters around you. Are you swimming in a crowded red sea, or is there a blue ocean on the horizon waiting for you to discover? The blue ocean approach urges you to be part entrepreneur, part explorer – to venture beyond the maps of existing market space. It might feel risky at first, but the potential payoff is a market all to yourself and a chance to define the future on your terms.

In practice, you don’t have to bet the farm all at once. You can incorporate blue ocean thinking gradually: carve out a unique feature here, target an overlooked segment there, and keep pushing in that direction. Over time, you might realize you’ve created an entirely new category. And that’s the dream for many startups – to be not just another player, but the leader of a space you’ve defined. As one entrepreneur’s mantra goes, “Don’t skate to where the puck is, skate to where it’s going to be.” Blue Ocean Strategy is about skating to where the puck isn’t yet, and being there waiting with your product when it arrives. Good luck!

At molfar.io, we help startup founders turn bold ideas into real products. From deep market research to smart product strategy and fast, lean MVP development — we help you validate, build, and launch with confidence. Ready to move fast and smart? Book a free consultation. Your startup journey starts here!